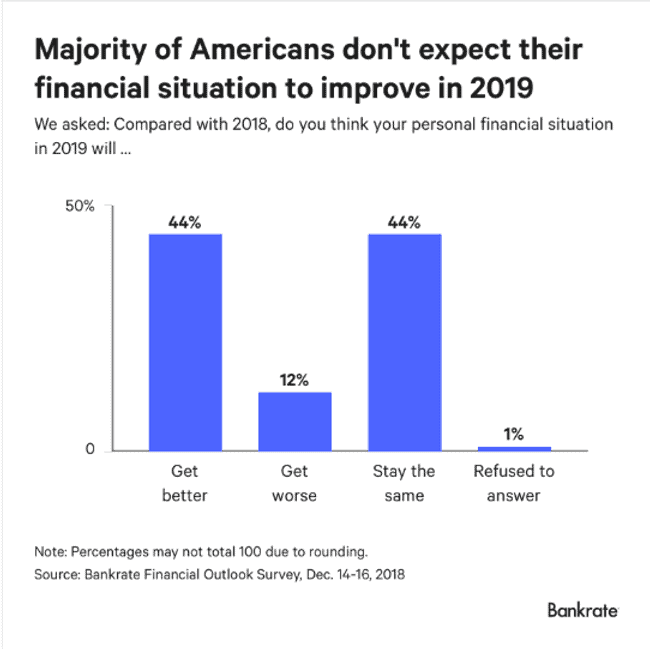

Most of us expect our finances to get better over time, as we advance in our careers and our income goes up. But heading into 2019, according to Bankrate’s most recent Financial Outlook Survey, 55% of Americans don’t expect their financial situation to improve. This number includes 12% percent who think their situation will be worse and 44% who think it will stay the same. Older respondents were more pessimistic compared to millennials, as were women compared to men.

When asked why, 49% blamed current political leaders in Washington, D.C. Other reasons included the higher cost of living (38%), and increased debt burden accounted for another 37%. In a separate survey, conducted in January 2019, only 40% of respondents reported that they would be able to meet a $1,000 financial emergency by accessing their own savings, with 30% having experienced just such an emergency in the past year of up to $5,000. Both surveys were conducted using representative samples of the US population as a whole.

These results are not surprising, given the financial fallout from the recent government shutdown and media speculation over its effects on an already slowing economy. However, Americans have been pessimistic about the overall economy and have held the government responsible for their personal financial struggles for much longer.

These results are not surprising, given the financial fallout from the recent government shutdown and media speculation over its effects on an already slowing economy. However, Americans have been pessimistic about the overall economy and have held the government responsible for their personal financial struggles for much longer.

A 2013 poll by the National Journal reported 62% of Americans at that time as holding the federal government responsible for having a negative influence on their individual financial situation. Reasons cited included fewer opportunities for changing jobs or for raises in a current job, higher interest rates, and more difficulty obtaining a personal loan.

Why do these kinds of beliefs matter? Such perceptions can become a self-fulfilling prophecy when they start to affect the choices people see as being available to them and the financial decisions they make as a result. Regardless of how rational their beliefs may be, they can influence how much money people choose to save or spend, or whether it’s worth it to ask for a salary increase or seek a better-paying job. In turn, these individual actions can collectively affect the larger economic picture—beliefs work both ways.

While it’s important to encourage plan participants to take steps to take action over the things they can realistically control, such as saving an emergency fund, it’s equally important for advisors to acknowledge that there are external factors beyond the participant’s control that can have a negative impact on an individual’s situation. For example, there is a real gender wage gap that affects women of color, which over the long term severely affects their ability to save adequately for retirement.

The current financial system has systematically shifted more risk to the individual, as the history of the 401(k) shows. Placing the onus for financial health solely on plan participants without noting how the larger economic picture may limit their ability to reach a state of financial well-being contributes to misconceptions about low-income workers and the perception that financial advice is only for the well-to-do.

Dr. Martha Brown Menard is the Senior Researcher and data diva for Questis. She is a research scientist, financial wellness coach, and member of the Association for Financial Counseling and Planning Education. She is passionate about democratizing personalized financial guidance through scalable and configurable technology.