Whenever I read another article about how hard it is to measure the ROI of financial wellness programs, I think back to my days as a psychology grad student. A large part of psychology and its history is focused on figuring out how to measure the intangible. The field of psychometrics measures abstract concepts such as intelligence, anxiety, and competence. And of course educators at all levels have engaged in assessing the effects of educational interventions, such as programs in financial literacy, for many years. There’s a great deal we actually do know about the costs of financial stress that can help us estimate the ROI of financial wellness. First, let’s understand a little more about how we can measure financial stress and its impact on a business.

Academics in the field of financial education and counseling, such as E. Thomas Garman, have been measuring the effects and costs associated with financial stress in the workplace for more than 20 years. Some measurement tools rely on what people say they think or do; these are self-report measures. Other tools rely more on what people actually do, based on direct observation of behavior or the results of behavior. Self-report measures are an effective way to quantify subjective experience, such as beliefs, opinions, and feelings, while behavioral measures are effective at quantifying objective changes in behavior. But before we can measure something, we have to describe and define it. We need an operational definition.

That’s one of the problems when it comes to estimating the ROI of financial wellness as an employee benefit. Financial wellness is a somewhat elastic term. Most experts agree that financial wellness is multifaceted, and a lot of people like the broad definition put forth by the Consumer Financial Protection Bureau, which is based on extensive research and includes both subjective and behavioral aspects. However, many of the tools offered by the increasing numbers of financial wellness providers focus on addressing only 1 or 2 issues in the bigger picture of comprehensive financial wellness. That’s not necessarily a bad thing. But it does make assessing the ROI of financial wellness more difficult when the term ‘financial wellness’ can mean many different things to different people. It’s not just comparing apples and oranges, it’s one big fruit salad.

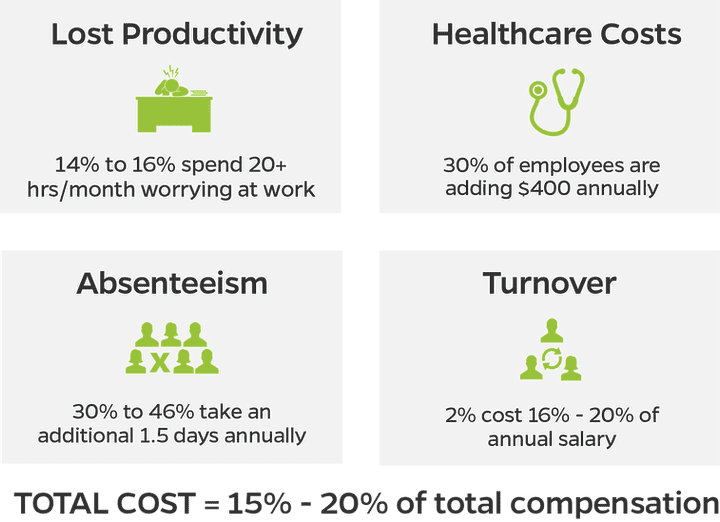

What does the existing research on financial stress tell us? We know that almost half of employees experience financial stress, and that financially stressed employees bring those issues to work with them, affecting their productivity. In the most recent PwC Financial Wellness Survey, 30% of workers said that finances are a distraction for them at work, and of those, 46% admitted that their productivity suffered as a result, spending 3 or more hours weekly dealing with financial issues at work. That’s 138 hours annually per stressed-out employee. Multiply that by the company’s blended hourly rate and costs stagger quickly. These numbers are consistent with what other academic researchers have found over the past 20 years.

Absenteeism and turnover rates offer additional quantifiable measures. Surveys have found that compared to non-stressed employees, financially stressed employees take off an additional 1.5 days from work annually to deal with financial issues. So, multiply that number by the 30% of employees at an individual company, times the blended hourly rate. Financially stressed employees are also more likely to leave for higher wages elsewhere. This means more turnover.

Turnover can be very expensive, and rates of turnover vary by industry. The cost includes the time and fees associated with recruitment, interviewing, screening, hiring, onboarding, and training, and increases as a percentage of salary paid. As a rough estimate, about 2% of lower and mid-range positions turn over every year, and 1% of upper salaried positions. For high-turnover, low-paying jobs (earning under $30,000 annually), the cost is only 16% of annual wages. For mid-range positions earning $30,000 to $50,000 annually, the cost increases to 20% of annual salary. For more complex senior or executive positions, the cost can range up to 213% of annual salary. For example, the cost to replace a $100k executive can be as much as $213,000, in part because it often takes longer for a new employee to get up to speed and be as productive, especially in more demanding roles.

Financial stress also affects employee healthcare costs, particularly for those conditions related to or exacerbated by stress. The CFPB estimates that financial stress can increase healthcare costs by about $400 per stressed employee annually.

“The CFPB estimates that financial stress can increase healthcare costs by about $400 per stressed employee annually.”

Taken together, these measurable costs add up. E. Thomas Garman and colleagues estimate that the total cost of financial stress in the workplace ranges from 15% to 20% of total compensation paid, including benefits. While additional factors influence productivity, absenteeism, turnover, and healthcare costs, incorporating a financial wellness benefit to reduce the costs associated with financial stress by even 3%-5% by can improve a company’s bottom line simply through cost avoidance.

THE HIGH COST OF FINANCIAL STRESS

“We know that education alone is not sufficient

to change financial behaviors.”

When a financial wellness tool addresses only one aspect of the total financial wellness picture, we need to look at more specific rather than global outcomes. We need to consider what the tool is intended to accomplish, and then measure the outcomes related to that goal(s). As noted previously, other factors can affect productivity, absenteeism, turnover, and healthcare costs. However, if we know many of a plan sponsor’s employees are struggling with student loans, we can look at whether or not progress is being made across the company on paying down student loan debt. We can also look at 401(k) loan rates. PwC has found that those earning less than $75,000 annually struggle more to meet financial needs, especially with using credit cards as a substitute for an emergency fund, and are more likely to raid their retirement savings to cover an unexpected expense or pay off accumulated credit card debt. So, in addition to reducing 401(k) loan numbers, we would also look for changes in the percentage of employees who have or are contributing to an emergency fund, and dollars of credit card debt being paid down.

Something I have learned as a scientist is that it’s much more important to measure what is meaningful than what’s easy to measure—like the joke about the drunken man looking for his wallet under the lamppost. When a passing police officer asks him about it, the drunk explains that he lost the wallet farther down the street, but he’s looking for it under the lamppost because ‘the light’s better here.’ When we only measure what’s easy instead of what’s meaningful, we’re making that same mistake.

For a meaningful assessment, it’s critical to look at more than numbers. Providing an authentic financial wellness benefit should improve people’s lives through helping them meet their individualized financial goals. Evaluating whether a financial wellness program is worthwhile should also include some assessment of the impact the program is having, as evidenced by individual narratives.

As more employees, particularly millennials, turn to their employers for help with managing challenging and complex financial issues, offering a comprehensive financial wellness benefit can help retain current employees and be an attractive recruiting tool for potential candidates. As the number of American employees quitting their current jobs to seek better ones hits an all time high, that’s a pretty good ROI in and of itself.

Dr. Martha Menard is the senior researcher and data diva for Questis, a financial wellness technology platform. She is a research scientist and current member of the Association for Financial Counseling and Planning Education.